UPM et Anker Schiffahrt prolongent leur contrat pour les opérations du terminal d'Emden

Dans le cadre d'une démarche renforçant l'un des plus longs partenariats logistiques dans le secteur de la pâte et du papier, UPM et Anker Schiffahrts ont renouvel&eac ...

Allemagne : Tricor mettra en service sa nouvelle onduleuse à Weeze mi-juillet

Pour mémoire, Tricor a investi environ 170 millions d'euros dans la construction de sa nouvelle usine ...

GCP Paper investit 400 M$ dans une usine de tissue au Texas

Le fabricant mexicain de tissue Grupo Corporativo Papelera (GCP) a amorcé la construction de sa première usine aux &Eacu ...

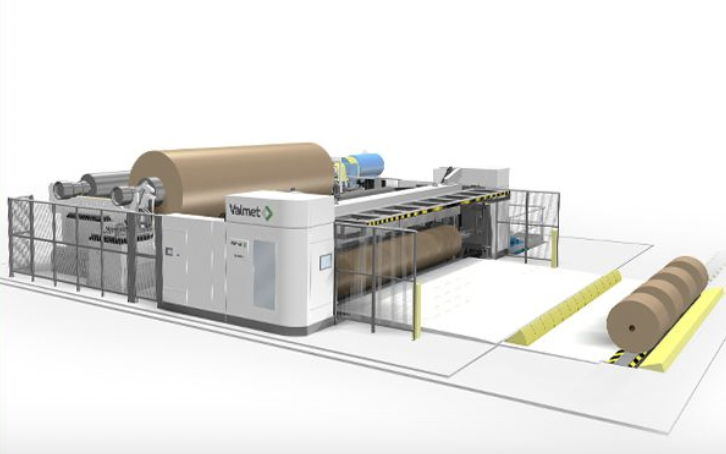

Chine : Valmet obtient une commande de technologie de pâte à papier pour Sun Paper

C'est un gros contrat que vient de décrocher le finlandais Valmet, qui a été charg ...

Cartiere Carrara va construire une nouvelle usine de tissue en Italie

Le fabricant italien de tissue et d'autres produits similaires, Cartiere Carrara, prévoit de construire une nouvelle usine ...

L'usine de pâte à papier d'Aspa Bruk se dote d'une nouvelle station d'épuration

Une nouvelle station d'épuration est en cours d'installation à l'usine suédois ...

Le groupe Metsä s'attend à un résultat d'exploitation négatif

Mauvaise nouvelle : Le groupe Metsä anticipe un résultat d'exploitation négatif pour le deuxième trimestre de cette année. Selon l'entreprise, c'est la faiblesse ...

Nordpack reprend l'usine de fabrication de cartons Coburger

Bonne nouvelle : Après la déclaration de cessation de paiement de Coburger Kartonagenfabrik début mars qui menaç ...

Ahlstrom reçoit une offre ferme de Munksjö pour son activité Abrasifs

Le groupe papetier finlandais Ahlstrom (6 800 salariés, 3 milliards d'euros de chiffre d'affaires) ...

Paprec et Decoset inaugurent à Bessières le plus grand centre français de tri des déchets ménagers recyclables

Pour plus d’un million d’habitants de la métropole toulousaine, le geste de tri va devenir encore plus performant. Paprec, leader français du recyclage et Decoset, le ...

Redémarrage de la production à l'usine Kemi de Metsä

Le groupe Metsä annonce que l'usine de pâte à papier de Kemi et l'usine de papier adjacente ont repris l ...

Le suédois PulPac bénéficie d'un prêt de 20 M€ pour promouvoir des alternatives aux plastiques à usage unique

La Banque européenne d'investissement (BEI) ...

Le gouvernement gallois investit environ 9,3 M€ à Wepa à Bridgend

Cet investissement de 8 millions de livres sterling (soit près de 9, 3 millions d'euros) du gouvernement gallois, sous forme de prêts, de prises de participation et de subventio ...

Chine : Nine Dragons Paper lance une nouvelle usine de pâte à papier dans le Hubei

C'est dans la province du Hubei, en Chine, dans l'usine intégrée de production de pâ ...

Palm renforce sa position sur le marché grâce à l'acquisition de 5 usines IP

Le groupe allemand Palm a validé l'acquisition de cinq usines d'emballages en carton ondul ...

Metsä Tissue supprime 93 emplois à l'usine de Kreuzau, en Allemagne

Metsä Tissue, filiale du groupe Metsä et l'un des principaux producteurs européens de tissue, a conclu ...

L'américain Packaging Corporation of America (PCA) reprend l'activité de carton ondulé de Greif

Décidément Big is beautiiful en ce moment aux USA et la consolidation des groupes va bon train. Cette fois-ci l'opération concerne PCA qui rachète Greif. Cette tran ...

Stepak Bourdin négocie pour acquérir Le Nappage et Sodipan Table

Le groupe familial sarthois Stepak Bourdin (80 M€ de CA en 2024, 250 collaborateurs), présidé par C&e ...

Le fabricant britannique d'emballages Krystals est placé sous administration judiciaire

Cette procédure entraine le licenciement d'environ 80 employés. Krystals opéra ...

Bulteau Développement acquiert le cartonnier CPL-OP emballages

Le groupe nanto-sarthois CPL-OP, spécialisé dans la transformation de carton ondulé pour des emballages sur-mesure et ses 4 sites de production rejoignent ainsi le nordist ...

Norra Skog investit 10,5 M$ dans la scierie Hissmofors en Suède

Le conseil d'administration de Norra Skog a décidé d'investir 100 millions de couronnes suédoises (10, ...

Label G2 acquiert Concept Étiquettes

Label G2 reprend l'imprimerie familiale Concept Etiquettes (1 M€ de CA), située à Amplepuis, par Label G2, installée près ...

Suzano avance vite dans la construction de sa nouvelle usine de Tissue à Aracruz, au Brésil

Avec un investissement de 650 millions de R$ (environ 115 millions USD), le projet avance com ...

Siegwerk rejoint Topac pour les emballages de tabac

Le fabricant allemand d'encres d'impression Siegwerk a rejoint Topac, une alliance dédiée à l'industrie de l'emballage du taba ...

USA : Sofidel finalise l'acquisition de plusieurs usines de tissue de Royal Paper

Le groupe papetier italien spécialiste des papiers d'hygiène et sanitaire (essuie tout, papiers hygiéniques) Sofidel continue son développement en Amérique d ...

Hubergroup augmente les prix de ses encres

Face à une hausse marquée du prix de la nitrocellulose, le fabricant allemand d'encres et de vernis pour impression, Hubergroup (743 M&eu ...

Södra s'associe à la société d'IA Terra Labs

En collaboration avec l'entreprise d'IA Terra Labs, Södra lance une initiative visant à garantir à ses m ...

4evergreen en visite chez Koehler Paper à Kehl

Des représentants de l'initiative européenne de l'emballage 4evergreen se sont rendus sur place pour découvrir la produ ...

L'autrichien Rondo Ganahl cède son usine de carton ondulé à Istanbul

Exit La Turquie ! L'entreprise autrichienne Rondo Ganahl a vendu son usine d'emballages en carton ondulé d'Istanbul, en Turquie, à un fabricant local. Cette décision ...

Et si Stora Enso cédait ses actifs forestiers suédois ?

C'est en tout cas à l'étude. Le géant finno-suédois envisage en effet une scission de ses actifs ...

Progroup démarre sa nouvelle usine d'alimentation de feuilles ondulées en Italie

Progroup, producteur allemand de carton ondulé et de feuilles ondulées, a franchi une étape importante dans sa nouvelle usine de Cessalto, près de Venise, en d ...

MM Premium va devoir adapter les capacités de production de son usine d’Ancenis

Le producteur d’étuis pour les cosmétiques et les spiritueux de luxe, filiale du group ...

Navigator utilise la méthodologie « Ten Toes » pour mesurer son empreinte carbone

The Navigator Company vient d’annoncer l’adoption de la méthode Ten Toes, ...

Norske Skog Skogn produira du papier pour livres à partir du deuxième trimestre 2026

Ce nouveau produit, baptisé NOR Book, sera décliné en différentes qualités standards de main, de blancheur et de teinte. Montant de l'investissement : enviro ...

Metsä Board ferme l’usine de Tako à Tampere

La production de l'usine de carton plat de Tako a pris fin le 17 juin, avec l'arrêt de la machine à carton BM1. Mets&au ...

La Fespa modernise son identité visuelle

« Notre nouveau look est frais, futuriste et apporte un nouveau niveau de clarté à la façon dont nous nous présentons ...

Un licencié PulPac met en service une ligne de production de fibres moulées à sec

Une de plus ! C'est dire le succès de cette technologie initiée par PulPac. La nou ...

Sofidel finalise l'acquisition des actifs de Royal Paper aux États-Unis

Avec ce rachat, Sofidel ajoute quatre nouvelles installations à ses opérations nord-américaines, consolidant ainsi un marché stratégique qui gén&egrav ...

Obeikan va fermer son usine d'emballage de Valence

Le groupe d'emballage saoudien Obeikan ferme son usine d'emballages en carton ondulé située près de Valence, en Espagne. L ...

OptiGroup rachète CreaPak, un distributeur finlandais d'emballages

En pratique, CreaPak, spécialisé dans les solutions pour les secteurs de l'agroalimentaire et du bâtiment, intégrera l'activité emballage d'OptiGroup en Finla ...

Le chilien CMPC ouvre un nouveau bureau à Atlanta pour renforcer sa présence en Amérique du Nord

Cap sur les Etats-Unis ! C'est la stratégie adoptée par de plus en ...

Et si c'était possible de créer un dispositif de diagnostic médical en papier par fabrication additive ?

C'est l'objet de la thèse d'Erwan Troussel (Grenoble INP-UGA), qu' ...

L'autrichien Lenzing Papier investit dans une nouvelle usine de désencrage

Sa mise en service est prévue au troisième trimestre 2025. Grâce à cet investissement, Lenzing Papier souhaite établir de nouvelles normes en mati&e ...

L'usine de papier Feldmuehle reprend sa production

Feldmuehle, fabricant de papiers pour étiquettes et d'emballages souples, en faillite, a relancé sa production de papier. Sa machine & ...

Canada : Produits Kruger a inauguré une nouvelle usine de tissue LDC à Sherbrooke

Elle est construite sur un site adjacent à son usine TAD. Dans le détail, la construction ...

Changement de nom pour UPM Raflatac

À compter du 12 juin, la division opérera sous le nom d'UPM Adhesive Materials. Ce nouveau nom sera utilisé dans les rapports financiers &agra ...

Communication visuelle : Antalis rachète Club groupe

Décidément Antalis ne chôme pas et continue son développement avec des opérations de croissance externe ! On rappelle que l'an dernier, Antalis a repris ...

Green Bay Packaging investit plus d'1Md $ dans son usine de papier kraft de l'Arkansas

Le groupe américain Green Bay Packaging, fabricant leader de solutions d'emballage, agrandit son usine de ...

Leader Paper Products acquiert Unique Envelope

Décidément, on parle beaucoup d'enveloppes en ce moment (à ce propos, ne manquez pas l'itv de GPV France dans le dernier numé ...

Solidus confirme son intention de fermer Bad Nieuweschans

Solidus, l'un des principaux producteurs de carton compact et des solutions d'emballages néerlandais, a confirmé son intention ...

Pap'Argus 423 est paru la semaine dernière

C'est Pascal Haeffner, Dg de GPV France qui fait la Une et qui, dans les pages intérieures du magazine, revient sur l'évolution du ...

MM Packaging Bangor est rebaptisé CB Paper Sacks

Ce changement de nom fait suite au rachat opéré plus tôt cette année : Le spécialiste des sacs multi-parois b ...

Le suisse Amcor fusionne officiellement avec l'américain Berry

C'est fait ! Le nouvel ensemble créé par le groupe australo-suisse Amcor et Berry est né : c'est l ...

Ahlstrom investit 15 M€ à Saint-Séverin pour installer une nouvelle ligne de production

Le groupe papetier finlandais Ahlstrom (6 800 salariés, 3 milliards d'euros de chiffre d'affaires) a inauguré fin mai dans son usine de Saint-Séverin une nouvelle lig ...

IP envisage la construction d’une nouvelle usine d’emballages durables à Salt Lake City

L'étude d'une nouvelle usine potentielle s'inscrit dans le cadre des plans de croissa ...

Le fabricant allemand d'emballages Weig s'implante sur le marché nord-américain

Cette initiative est menée par sa division Weig Europack et sera mise en œuvre en étr ...

Shotton Mill modernise son four et signe un accord de service avec Valmet

Le finlandais Valmet a signé un contrat pour la modernisation du four à Shotton Mill, au Royaume-Uni. Ce p ...

Metsä Fibre achève les négociations sur le chômage technique à Rauma et Joutseno

Le fabricant finlandais de pâte à papier et de produits en bois Metsä ...

Schönfelder Papierfabrik inaugure une nouvelle centrale de cogénération biomasse

Schönfelder Papierfabrik investit dans la décarbonation de sa production d'énergie : début mai, l'entreprise a inauguré une nouvelle centrale de cog& ...

Un feu s'est déclaré dans une cellule de stockage du site de Saica Paper Laveyron

Plus de peur que de mal, néanmoins, l'incident a été spectaculaire. C'est en ces t ...

Van Genechten Packaging investit dans son usine VG Kvadra Pak JSC en Lettonie

Le fabricant de boîtes pliantes VGP prévoit d'investir un total de 10 millions d'euros dans son us ...

UPM Specialty Papers investit 10 M€ dans son usine de Tervasaari

UPM Specialty Papers modernise son usine de papiers spéciaux de Tervasaari, à Valkeakoski, en Finlande. Ce chantier de 10 millions d'euros permettra à l'entreprise d'augme ...

La brique alimentaire débarque sur les réseaux sociaux

L'agence Edelman signe “C’est dans la brique !”, la nouvelle campagne de communication d’Alliance Carton N ...

La Métropole de Rouen écrit au ministre de l’Industrie au sujet de Chapelle Darblay

C'est trop long ! La pression monte du coté de Chapelle Darblay ! Alors que le délai de cinq mois octroyé fin 2024 arrive à son terme fin mai, la reconversion (pour ...

Wepa va augmenter sa capacité de production au Royaume-Uni

Nouveau projet pour Wepa, qui va installer une nouvelle machine à papier à Bridgend au Royaume-Uni. Le programme, qui c ...

Mondi étend la capacité de re/cycle MailerBAG

Mondi accroit sa capacité de production de MailerBAG re/cycle afin de répondre à la demande croissante de solutio ...

Navigator investit 30 M€ pour convertir sa MAP 3 à Setubal

Avec ce programme d'investissements, le portugais Navigator Company veut renforcer son engagement dans la production de papiers d'emballage souples à faible grammage. Le dém ...

International Paper (IP) prévoit de fermer cinq de ses sites d'emballage au Royaume-Uni

Au total, environ 300 postes pourraient être concernés. Les mesures proposées compre ...

Allemagne : Le groupe Peters ferme Cartonia Wellpappen fin septembre

Le groupe Peters souhaite renforcer sa position et se concentre sur six sites. Cette stratégie signifie égaleme ...

Etats-Unis : Valmet va fournir une rénovation complète de la MAP 2 de Sylvamo

Il s'agit précisément de la MAP 2 de Sylvamo située à Eastover, en Carolin ...

La PME iséroise Allimand sort du plan de sauvegarde grâce à Arcole

Ce n'était pas une mince affaire que de retrouver le chemin de la rentabilité ! Mais le fabricant de machines à papier Allimand, après deux années de re ...

Citeo alerte sur les dérives de la REP Emballages ménagers

Trop c'est trop ! Pour l'éco-organisme Citeo, la REP Emballages ménagers est devenue, au fil du temps, un s ...

Rottneros va licencier moins que prévu

Rottneros va supprimer des emplois en Suède, mais pas autant qu'annoncé : Les négociations étant désormais finali ...

La nouvelle onduleuse d'Aquila en Pologne est opérationnelle

Le fabricant polonais de carton ondulé Aquila, filiale du groupe belge VPK, a installé une nouvelle onduleuse dans so ...

Norske Skog Golbey a produit sa première bobine de papier d’emballage

Elle était attendue cette première bobine ! Enfin ! Norske Skog Golbey a produit cette semaine sa première bobine mère de papier pour ondulé. Pour mém ...

Le producteur allemand de papier d'édition Kabel Premium Pulp & Paper cesse ses activités. L'administrateur judiciaire de l'entreprise, placée sous administration ...

Stora Enso cède 12,4 % de ses actifs forestiers en Suède

Comme annoncé en octobre dernier, le groupe suédois de papier et d'emballage va céder 12,4 % de ses ac ...

En valeur, le numérique représentera 22,5 % du marché de l'impression et de l'emballage imprimé en 2035

Dans le secteur de l’impression, la technologie num&eacu ...

Mission accomplie pour Imprim'Luxe, qui rassemble les industriels français concepteurs, fabricants et imprimeurs de supports multilatéraux. Le premier Forum du Print et du Packag ...

DS Smith a breveté une enveloppe réemployable en papier-carton

La substitution du plastique par le papier carton donne lieu à toujours plus d'innovations et le mérite de l ...

L'américain Packsize rachète son concurrent néerlandais Sparck Technologies

Packsize acquiert auprès de Standard Investment Sparck Technologies, un fabricant europ&ea ...

Au sommaire, une ITV du Pdg de Général Emballage, Ramdane Batouche, un cahier technique qui détaille comment le papier pour étiquettes est le premier vecteur de r&e ...

USA : ABB conclut un deal avec Raumaster Paper

ABB annonce que la société a signé un protocole d'accord avec Raumaster Paper visant à explorer conjointement des solut ...

Rengo acquiert Shinko au Japon

Shinko a été fondée en 1953 sous le nom de Shinko Shiki et se consacre depuis à la fabrication et à la vente de matériaux d'em ...

Les cendres papetières deviennent un co-produit à la fabrication de ciment décarboné

Décidément, nous ne sommes pas au bout de nos surprises avec le papier ! C'est véritablement un matériau bourré de qualités et ce nouveau partenariat ...

Georgia-Pacific va fermer l'usine de carton de Cedar Springs en Georgie

La plupart des postes seront supprimés d'ici le 1er août 2025. Environ 535 emplois seront impactés par cett ...

Une IA de Springer Nature détecte les fraudes dans la littérature scientifique

Son nom ? Gepetto. Le développement de cette IA est une démarche vertueuse à l'initia ...

Gulf Paper Manufacturing lance une ligne de production de mouchoirs dans son usine de Mina Abdullah au Koweït

Gulf Paper Manufacturing et Toscotec ont démarré la MAP 2 apr&egr ...

International Paper va fermer deux usines au Texas

International Paper a annoncé la consolidation de ses opérations dans la vallée du Rio Grande le long de la frontiè ...

Stora Enso a conclu un partenariat avec Oppboga Bruk

Stora Enso collaborera avec le suédois Oppboga Bruk (groupe Kapag) pour la production et la commercialisation d'Ensocoat 2STM à ...

Pulpac accueille 2 nouveaux actionnaires, SIG InnoVentures et Optima

PulPac annonce l'arrivée de SIG InnoVentures et d'Optima, leader mondial des technologies de pointe pour les machines d'emballage, en tant que nouveaux actionnaires. Cela té ...

Le papetier italien Fedrigoni va ouvrir un centre de découpe en Allemagne

Toujours très dynamique, l'italien Fedrigoni annonce l’ouverture, au quatrième trimestre 2025 ...

Greif va fermer définitivement son usine de carton à Los Angeles

L'usine de Los Angeles devrait cesser ses activités en juin 2025. L'usine, qui produit du carton recycl&eacu ...

Hartmann Packaging et Dentaş Kağıt Sanayi acquièrent Dentaş Roumanie

Fondé en 2004 et basée à Tărtăşeşti, dans le département de Dâmboviţa, Dentaş R ...

Matías Gomá Tomás augmente la capacité de production CCM en Espagne

Le groupe technologique allemand Voith a reçu une commande du fabricant espagnol de carton ondulé Matías Gomá Tomás pour la modernisation de la machine &agra ...

Metsä Fibre prévoit du chômage technique sur ses sites à Joutseno et à Rauma

Metsä Fibre, filiale du groupe Metsä, va entamer des négociations concern ...

Les nouvelles exigences de gestion forestière durable PEFC pour la France entrent en vigueur

Ce sont plus de 100 exigences qui se traduisent par 31 engagements, dont 9 évolutions princi ...

Amcor investit 13 millions d’euros dans son usine alsacienne

Du nouveau en Alsace ! A Ungersheim, près de Mulhouse (Haut-Rhin), sur le site appartenant à Amcor, va être ...

Le salon du grand format organisé par Fespa est lancé sous le soleil et le moins que l'on puisse dire c'est que non seulement le carton est à l'honneur mais l'emballa ...

Asia Symbol cartonne dans la production de boîtes en carton pliante grâce à Voith

Le partenariat entre Voith et Asia Symbol, un important producteur mondial de pâte &agr ...

L'allemand Remondis entre dans le capital du groupe strasbourgeois Schroll

C'est un changement important pour Schroll, acteur de référence dans la gestion et la valorisation des d&eacut ...

Kimberly-Clark veut investir plus de 2 Mds de $ pour développer sa production aux États-Unis

Effet Trump... ou pas ? En tout cas, l'annonce est d'importance : Kimberly-Clark décide d'investir plus de 2 milliards de dollars au cours des cinq prochaines années dans se ...

Smurfit Westrock va réduire sa capacité de production en Allemagne et aux États-Unis

Le groupe international de papier et d'emballage Smurfit Westrock ferme des usines aux &Eacut ...

Bureau Vallée table sur des tarifs des fournitures et matériels scolaires en légère baisse

J - 5 mois avant la rentrée scolaire ! Dans un contexte économique ...

Mondi démarre sa machine de production de carton recyclé à Duino

Mondi a mis en service sa machine de production de carton ondulé recyclé reconstruite sur son site de Duino, en Italie. Une fois pleinement opérationnelle, la machine ...

Nordic Paper approuve des investissements pour Bäckhammar pouvant atteindre près de 41 M€

Nordic Paper a décidé aujourd'hui d'approuver des investissements environ ...

Amcor et Berry reçoivent le feu vert de la CE pour leur rapprochement

C'est ok : Le groupe australo-suisse Amcor a l'autorisation antitrust de la Commission européenne (CE) de racheter son homologue américain Berry. La transaction devrait être finali ...

Natron-Hayat va reconstruire sa MAP 1 et introduire une nouvelle qualité de papier kraft mixte

Natron-Hayat, producteur sud-est-européen de sacs et de papier kraft, va reconstruire ...

Voith modernise la MAP 1 de Matías Gomá Tomás en Espagne

L'objectif de cette rénovation est d'améliorer la qualité du papier et d'augmenter la capacité ...

Le groupe coopératif Alkor (enseignes Majuscule, Burolike et Ioburo) avait eu la préférence du tribunal de commerce de Lille pour la reprise d'Office Depot, plac&eacu ...

Allemagne : Niederauer Mühle augmente ses tarifs pour les papiers ondulés

Ces augmentations s'appliqueront à compter du 1er mai 2025. Les hausses de prix massives des vieux papiers ...

Japon : Rengo investit dans Kinki Danboru

Rengo, leader du secteur de l'emballage et premier fournisseur de boîtes en carton ondulé au Japon, annonce avoir investi dans Kinki Danboru. C' ...

Le finlandais Huhtamaki acquiert Zellwin Farms en Floride

Huhtamaki a racheté Zellwin Farms, une entreprise privée située à Zellwood, en Floride, aux États-Uni ...

Après Zetacarton et Iemme Packaging, le groupe VPK, dirigé par Pierre Macharis, continue de compléter ses activités en Italie en acquérant Open Imballag ...

Norske Skog finalise la vente de l'usine de papier d'édition Boyer

Norske Skog a conclu la vente de son usine de papier journal et de papier LWC de Boyer, en Tasmanie, à Boyer Capital, ...

Nefab acquiert Embalajes Echeberria

Le groupe Nefab rachète l'entreprise basque Embalajes Echeberria Soluciones de Embalaje, spécialisée dans les solutions d'emballage compl ...

L'imprimeur de billets de banque De La Rue est repris par le fonds d'investissements américain Atlas

Changement d'actionnaire pour l'imprimeur fiduciaire britannique De La Rue ! Il est repris par le fonds d'investissement américain Atlas. Montant de la transaction : 263 millions d ...

Stora Enso rachète la scierie de Junnikkala

Dans le détail, les activités de la scierie finlandaise de Junnikkala vont être entièrement intégrées &agra ...

La complexe équation du recyclage chimique selon un rapport du cabinet E-Cube Strategy Consultants

Principal concurrent du papier-carton, le plastique est beaucoup moins recyclé que son ...

Suède : SCA signe des contrats de service avec Andritz pour son usine d'Östrand

Le groupe Andritz s'est vu attribuer d'importants contrats de service par SCA pour améliorer le ...

Chine : A.Celli va fournir une nouvelle bobineuse à papier à Five Continents Special Paper

Le partenariat entre Five Continents Spécial Paper et A.Celli se poursuit avec la ...

400 M€ pour décarboner l'industrie

C'est un plan ambitieux que se fixe le gouvernement français. Malgré le contexte économique tendu, il annonce un programme d'invest ...

Elopak entend doubler son chiffre d'affaires d'ici 2030

Elopak, l'un des principaux fournisseurs de briques alimentaires, a de fortes ambitions ! L'entreprise vise les 2 milliards d'euros de chiffre d'affaires d'ici 2030. Il est vrai que l'ann&eacu ...

Saint Domingue : Toscotec va équiper César Iglesias d'une ligne de production de mouchoirs

Toscotec (groupe Voith) va fournira une ligne de production tissue AHEAD 1.8 au groupe C& ...

L'espagnol Ence accélère sa transformation en fabricant de cellulose spéciale

Energia y Celulosa, leader européen de la production de pâte à papier d’eucalyptus, s’attend à ce que d’ici 2028, plus de 60 % des ventes de l&rsqu ...

Mitsubishi HiTec Paper Europe veut revitaliser son usine de Bielefeld pour la rendre compétitive

De la transparence avant tout : c'est ce que dit le communiqué officiel de Fujitaka Mizu ...

Arauco dévoile un projet d'usine de pâte à papier de 4,6 Mds de $ au Brésil

Grosse annonce du géant chilien de la pâte et du papier Arauco ! Il lance la construction de son projet Sucuriú, une nouvelle usine de pâte à fibres court ...

Démarrage réussi du plus grand pulpeur à tambour Andritz FibreFlow en Inde

L'Inde est un pays qui compte de plus en plus, y compris pour notre filière. il suffit de voir & ...

Procos s’installe à Milan

Le luxe à l'italienne fait rêver... Et motive les fabricants de packaging de luxe, à l'instar de Procos, à inaugurer un nouveau burea ...

SCA augmente les prix du papier Kraftliner brun et blanc en Europe

Les hausses de prix continuent et SCA annonce une nouvelle augmentation, du papier kraftliner brun et blanc en Europe. Le nouve ...

Voith modernise la MAP 3 chez Smurfit Westrock Navarra pour améliorer la qualité du papier MG

Le groupe Voith a reçu la commande pour la modernisation de la MAP 3 de Smurfit ...

Dynamique et innovante, voici les deux maitres-mots de La Rochette Cartonboard, spécialiste historique du carton plat à base de fibres vierges et propriété du fonds ...

L'industrie espagnole du carton ondulé augmente sa production en 2024

Selon l'association professionnelle AFCO (Asociación Española de Fabricantes de Envases y Embalajes de Cart& ...

L'allemand Palm veut racheter 5 usines de carton ondulé de l'américain IP

Dans le cadre de l'acquisition de DS Smith, International Paper (IP) doit se séparer de certains sites, notamment trois de ses usines normandes, pour suivre les recommandations de ...

Inauguration chez Fortissue de la 1ère machine à tissue au monde 100 % électrique

Belle collaboration que celle du fabricant portugais Fortissue et de Toscotec. Ce partenariat a ...

Cenpa n'a toujours pas trouvé de repreneur

Le producteur français de carton pour mandrins Cenpa, propriété du fonds allemand Accursia Capital, n'est toujours pas sorti d'a ...

Inde : ITC annonce l'acquisition de Century Pulp & Paper

ITC a signé aujourd'hui un accord pour le rachat de Century Pulp and Paper (CPP) auprès d'Aditya Birla Group. CPP, situ&eacu ...

Le FSC prolonge la suspension du processus de recours d'APP

Le FSC prolonge jusqu'à fin juin 2025 la suspension du protocole d'accord d'Asia Pulp and Paper (APP) relatif à la mise ...

Saica lance en Espagne sa nouvelle usine d'emballages en carton ondulé

Le groupe espagnol d'emballages Saica est en train de démarrer sa nouvelle usine d'emballages en carton ondulé à Sant Esteve Sesrovires, près de Barcelone, en Espag ...

Metsä Tissue va arrêter de traiter des fibres recyclées dans l'usine de papier de Mänttä

Metsä Tissue prévoit également d'entamer prochainement des ...

Ahlstrom investit sur son site à Lalinde

La substitution du papier au plastique est tendance et cela conforte le business du fabricant d'emballages Ahlstrom qui exploite sur le site de La ...

Le consortium Mavco Investments et Avenue Capital Group finalise le rachat de Hubergroup

Du changement en perspective pour le chimiste allemand spécialisé dans les encres et produits d' ...

Sofidel conclut une OPA pour acquérir certains actifs de Royal Paper

Le groupe italien Sofidel, leader mondial de la fabrication de papier hygiénique et domestique, notamment connu en Italie et en Europe pour sa marque Regina, signe un accord portan ...

Lancement de The Fespa Foundation

Fespa a annoncé la création de The Fespa Foundation, une organisation associée dédiée à la promotion de pratiques dura ...

Mayr-Melnhof Karton a terminé l'année avec des résultats solides

En 2024, ses ventes et son bénéfice d'exploitation ont été respectivement de 4,1 milliards d'euros (-2 % en glissement annuel) et de 190 millions d'euros (-17 %). L ...

Mitsubishi HiTec Paper va supprimer des emplois sur son site de Bielefeld

Le papetier japonais se penche sur le cas de sa filiale allemande et prend une décision drastique. Le fabricant M ...

Antalis poursuit sur sa lancée et rachète Fortuna Digital

Fondée en 1990, Fortuna Digital s'est imposée comme un leader régional dans le secteur de l'impression numérique. Présente dans plusieurs pays europée ...

Des licenciements sont prévus chez Valmet

Valmet prévoit de renouveler son modèle opérationnel afin de mieux servir ses clients et d'accroître son efficacit&eac ...

Gascogne a remonté la pente sur le second semestre 2024

Un chiffre d'affaires annuel en baisse de 4,9 %, mais dans ce contexte compliqué cela reste un bilan correct pour le groupe Gasco ...

Valmet signe un accord de service avec Saica Paper UK

Valmet et Saica Paper UK ont signé un contrat de service visant à garantir la disponibilité et les performances de la l ...

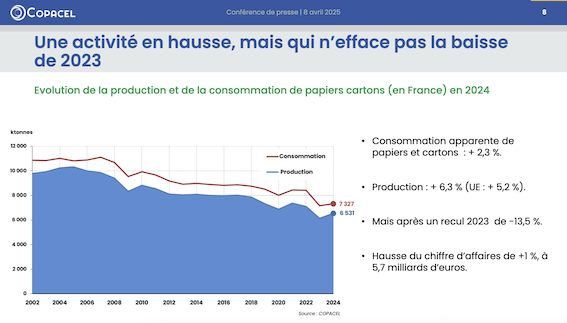

Bilan Copacel : La filière papier-carton affiche une activité en hausse, mais qui n’efface pas la baisse de 2023

La conférence de Copacel qui s'est tenue ce matin, aurait pu démarrer sur une note positive, la consommation des papiers et cartons en France ayant enregistré une progress ...

Quid de l'impact de la guerre commerciale sur la filière papier-carton ?

Pour les pâtes, papiers et cartons, aucun droit de douane n'était établi entre l’UE et les US ...

Sappi Europe augmente ses tarifs

Sappi Europe prévoit d'augmenter les prix de ses papiers spéciaux de 8 % pour les livraisons à partir du 15 avril 2025. La gamme comprend de ...

Le fabricant de sacs en papier Tapiero va déménager dans une nouvelle usine

Tapiero a le vent en poupe ! Le fabricant va déménager dans une immense usine de 10.000 m& ...

L'information avait fuité lors de la Nuit du papier du 3 avril organisée par Pap'Argus : Hervé Poncin, Ceo d'Antalis International et personnalité de l'industrie pa ...

Paprec Energies va capter le CO2 sur l’usine de valorisation énergétique de Pontivy

Paprec Energies installera sur cette usine, conçue par le groupe, un système perm ...

Tageos inaugure un centre d'innovation à Munich

Du nouveau chez le fabricant d’étiquettes connectées Tageos : le montpelliérain, filiale du papetier italien Fed ...

Andritz reprend A.Celli Paper

Encore des rachats dans le secteur ! Cette fois, c'est le groupe technologique international autrichien Andritz qui a signé un accord pour l'acquisition de l ...

Sonoco va fermer son usine d'emballage RTS Packaging à Scarborough dans le Maine

Sonoco annonce la fermeture de son usine d'emballages RTS de Scarborough, dans le Maine, d'ici fin juin 20 ...

Syndicats : Accord conclu dans l'industrie papetière finlandaise

Le syndicat finlandais des travailleurs du papier Paperiliitto et l'association des entreprises du secteur forestier finlandais Metsateollisuus ont conclu une convention collective valabl ...

Suzano augmente les prix de la pâte à papier en Asie, en Europe et en Amérique du Nord à partir d'avril

Le fabricant brésilien Suzano, premier producteur mondial de ...

L'américain Sonoco finalise la cession au japonais Toppan de ses emballages thermoformés et souples

1,8 milliard $ : c'est le montant de la cession par Sonoco de son activité ...

Novolex finalise son rapprochement avec Pactiv Evergreen

La transaction est évaluée à environ 6,7 milliards de dollars. Basée à Charlotte, en Caroline du Nord, la s ...

MPH1865 se dote du 1er gaufreur Touch Max sur une ligne industrielle en France

MPH1865 (ex MP Hygiène), leader français de la fabrication et de la transformation de produits d'hygi&egra ...

Plus de la moitié des Français lisent les étiquettes pendant leurs courses

56 % des français rapportent lire, pendant leurs courses, les étiquettes et les emballage ...

Lessebo Paper améliore sa conformité EUDR grâce aux tests "Traces"

Lessebo Paper AB poursuit sa démarche proactive pour garantir sa pleine conformité avec le futur R ...

Suite à la hausse des coûts du papier recyclé, Sonoco et Solidus Solutions ont annoncé des hausses de prix pour leurs produits, dont le carton pour mandrins. Da ...

The Navigator Company examine la conversion de l'usine de papier de Setúbal

Démarrage de la pré-ingénierie pour la reconstruction d'une machine à papier dans l'usin ...

A.Celli acquiert Sipack

Italia Technology Alliance, holding familiale du groupe A.Celli, élargit son portefeuille d'entreprises et acquiert Sipack, une entreprise lucquoise spécialis&ea ...

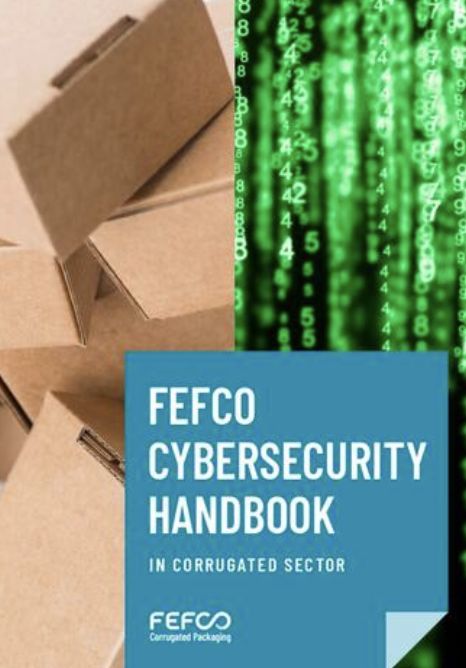

La Fefco publie un manuel de cybersécurité

La Fédération européenne des fabricants de carton ondulé (Fefco), a annoncé la publication de la premi&egra ...

Cartonnerie Moderne, Défi Imprimerie et Alpes Emballages pourraient passer sous le contrôle du groupe Guillin

Opération de croissance externe pour le groupe familial dirigé par Sophie Guillin. Le groupe Guillin, réputé pour ses emballages plastiques, poursuit ainsi sa ...

HolyPoly a obtenu une licence d'Andritz pour collecter et recycler les revêtements de machines à papier usagés (PMC) des usines à papier

Le groupe Andritz vient de sig ...

La grève de cinq semaines dans les usines UPM Plywood en Finlande se poursuit

Aucune solution n'a été trouvée dans le conflit de travail qui oppose UPM Plywood et le ...

Changement de gouvernance chez Cartonnages de Gascogne

Ce départ de la dirigeante était une étape planifiée avec l'arrivée en 2024 du groupe Atria (Cartonnages ...

Mondi a le feu vert de la Commission européenne pour acquérir Schumacher Packaging

La concentration dans le carton ondulé est de mise et le groupe sud-africain Mondi se rapproche de l'acte final de son projet de rachat de plusieurs usines d'Europe occidentale de ...

Mentorat : Hinojosa lance la troisième édition de Graduates

Graduates propose un accompagnement sur mesure et un suivi continu grâce au programme de mentorat. Avec ce programme,&n ...

Kipas Kagit démarre une nouvelle machine à carton ondulé à Söke

La nouvelle machine de production de carton ondulé, la MAP 3, de Kipas Kagit, installée à l'usine de Söke en Turquie, est désormais opérationnelle, apr& ...

Rottneros réduit la voilure

Rottneros a émis un avertissement sur ses résultats en raison de la hausse des prix des matières premières, de la baisse de la demande m ...

Papeteries d'Espaly pourrait supprimer 34 postes

Sur la base du volontariat, le fabricant d’emballages en carton ondulé basé en Haute-Loire a annoncé sa volonté de s ...

Saica investit dans de nouveaux équipements sur son site de Wigan au Royaume-Uni

Le groupe espagnol de papier et d'emballage Saica a annoncé un investissement de 7,1 millions d'euros (6 millions de livres sterling) sur son site de Wigan, au Royaume-Uni, afin de ...

L'usine de papier Feldmuehle annonce des prix plus élevés

Le fabricant de papiers pour étiquettes et de papiers d'emballage flexibles Feldmuehle a annoncé un ajusteme ...

Norske Skog Golbey commencera à produire du carton recyclé en avril

La production de carton ondulé recyclé à Golbey, c'est imminent ! Les équipes sont dans les starkings blocks et effectuent les derniers préparatifs sur le si ...

Bientôt une 10ème ligne de transformation sur le site de Lucart à Laval-sur-Vologne

Fin 2024, Lucart a signé une commande pour l'installation d'une nouvelle ligne de t ...

2024 ? Une année à oublier pour la Fipec

Mieux vaut oublier 2024 et penser à 2025... Sauf que 2025 ne s'annonce pas non plus sous les meilleurs auspices. C'est en substance le co ...

Cellulose moulée : une nouvelle ligne de production pour Ecofeutre

Ecofeutre, spécialiste des emballages en cellulose moulée, a inauguré sa nouvelle ligne de production en cellulose moulée sur son site du Sourn, venant complé ...

Greif annonce une augmentation de prix pour le carton recyclé non couché

Greif, spécialiste des produits et services d'emballage industriel, a annoncé une augmentation de ...

Kemira investit dans la production de produits chimiques pour le papier et le carton en Thaïlande

Kemira investira plusieurs millions d'euros dans l'extension de plusieurs lignes de product ...

La Cepi appelle la CE à poursuivre les négociations sur les tarifs douaniers américains

Il faut négocier. C'est le mot d'ordre de la Cepi qui pousse dans ce sens la Commission européenne. Car sans nul doute, l'imposition de droits de douane à l'importati ...

Carton Ondulé de France prône un langage de vérité

Des vertes et des pas mures ! On imagine combien Carton ondulé de France a du mal avec le discours de certain ...

Montée en puissance de la nouvelle ligne de carton de Stora Enso à Oulu

La ligne aura une capacité de production de 750 000 tonnes par an de carton pour boîtes pliante ...

Navigator envisage de convertir sa MAP 3 de l'usine de Setúbal

Le portugais Navigator s'apprête à convertir la MAP 3 de son usine à Setúbal, passant d'une produ ...

Bonne nouvelle ! Kabel Premium Pulp & Paper a redémarré l'une des deux machines à papier de l'usine de Hagen. Le fabricant de papier LWC et MWC avait en effet d&e ...

Finalement, la vaisselle en plastique reste bien interdite dans les cantines

Un rétropédalage de plus à l'actif du gouvernement. Cette fois, il s'agit de la vaisselle dans les ca ...

The Navigator Company va augmenter ses tarifs à compter du 1er avril

La société portugaise The Navigator Company s'apprête à augmenter les prix de vente de sa g ...

Stora Enso améliore sa capacité de production grâce à son partenariat avec Bobst

Les deux usines de transformation de Stora Enso Packaging, situées à Skene et ...

Paperfast s'associe à Fedrigoni

Paperfast, filiale italienne du groupe allemand de négoce de produits forestiers Jacob Jürgensen, a annoncé un partenariat stratégique ...

Extension des capacités chez Faller Packaging

À l’automne 2024, le spécialiste des emballages a fait l’acquisition de l’ancienne usine All4Labels à Gebes ...

L'usine de papier Aviretta n'est pas affectée par la fermeture d'UPM à Ettringen

Le fabricant de carton ondulé recyclé Aviretta, basé à Ettringen, a confirm& ...

Köhlerpappen est en cessation de paiements

Le producteur allemand de carton compact Köhlerpappen, qui affiche plus de 150 ans au compteur, rencontre des difficultés. L'entreprise est ...

Felix Schoeller augmente les prix des papiers décoratifs

Le fabricant allemand de papiers spéciaux Felix Schoeller appliquera une augmentation de prix allant jusqu'à 10 % sur ses ...

Saica annonce un deuxième investissement aux USA de plus de 110 M$

Avec un investissement de plus de 110 millions de dollars, le groupe Saica, l'un des acteurs européens les plus importants et les plus avancés dans le développement et la ...

Ence investit 14 M€ dans son usine de Navia

L'entreprise espagnole de pâte à papier et d'énergie Ence Energía y Celulosa prévoit d'accroître son effi ...

Teréga et Fibre Excellence s’associent autour d'un projet de captage de CO2

L'étude de faisabilité a été concluante et les deux parties sont donc tombé ...

Oji Holdings acquiert une société de fabrication de cellulose microcristalline en Inde

Oji annonce l'acquisition de Chemfield Cellulose Private, un fabricant indien de premier plan de c ...

Kabel Premium Pulp & Paper se déclare en cessation de paiements

Le producteur allemand de papier pour publications Kabel Premium Pulp & Paper vient de déposer une demande de cessation de paiements. Le tribunal de grande instance de Hagen a ...

La production à l’usine de Tako de Metsä Board devrait cesser d'ici la fin du 2ème trimestre

Metsä Board a finalisé les négociations de restructuration pou ...

Lancement du 66ème Cadrat d'or

La CCFI, Compagnie des chefs de fabrication des industries graphiques, sous l'égide de sa nouvelle présidente, Isabelle Erb-Polouchine organis ...

La Poste danoise cessera de distribuer le courrier fin 2025

En conséquence, le groupe PostNord va supprimer un tiers de ses effectifs. Soit 1500 sur 4500. PostNord justifie la r ...

Ticket de caisse électronique : nouveau cas de greenwashing

Heureusement que Two Sides est là pour pointer les nombreux cas de Greenwashing qui existent en France. Cette fois cela ...

Chômage technique : Fin des négociations de Metsä Fibre dans les scieries de Lappeenranta, Renko et Vilppula

Les négociations menées dans les scieries Metsä Fibre de Lappeenranta, Renko et Vilppula sur d'éventuels licenciements temporaires d'une durée maximale de ...

Belgrade : A.Celli modernise la machine à papier de l'usine d'Umka

A.Celli a été choisi pour reconstruire la section presse de la machine à papier de l'usine d'Umka & ...

Buckman est repris par le fonds d'investissement Pritzker Private Capital

Pritzker Private Capital, un leader de l'investissement direct familial, a annoncé la signature d'un accord définitif pour acquérir Buckman, une entreprise familiale innov ...

Produits Kruger lance sa nouvelle division Kruger pro

Produits Kruger, le principal fabricant canadien de produits de papier au Canada, a annoncé le lancement de sa nouvelle division, Kru ...

Groupe Verpack étrenne un nouveau site en Tunisie

C'est le sixième site de Verpack qui est installé précisément à Sousse. Les 5 autres (Paris, Touraine, Bour ...

Arctic Paper affiche un bilan mitigé

Le quatrième trimestre 2024 n'a pas été excellent pour le groupe suédois Arctic Paper, en particulier dans le segment de la p&a ...

Ce changement de nom marque son intégration au sein du groupe international OVOL Japan Pulp & Paper Group. Sa filiale spécialisée dans la communication visuelle, ...

Bong résiste et poursuit sa stratégie de transformation

Le groupe Bong a publié ses résultats pour l'exercice clos le 31 décembre 2024. Pour l'ensemble de l'an ...

Pap'Argus organise la troisième édition de la Nuit du Papier le jeudi 3 avril 2025, au Cercle National des Armées, Paris 8e. Sur le modèle des années préc&eac ...

Perlen Papier augmente ses tarifs

Le producteur suisse de papier d'édition Perlen Papier devrait augmenter ses prix de vente du papier journal au deuxième trimestre. On parle d'une ...

Canada : Arrêt de production temporaire d’une partie de l’usine WestRock de La Tuque

L'usine Smurfit WestRock de La Tuque fait cesser la production d'une de ses machines pendan ...

Bureau Vallée voit son CA progresser de 3,4 % en 2024

Joyeux anniversaire à Bureau Vallée qui fête ses 35 ans cette année et qui peut se féliciter d'une ...

Burgo envisage d'augmenter les prix du papier sans bois

Le groupe Burgo a annoncé une augmentation des prix du papier fin. La société italienne a annoncé qu'elle augmenterait jusqu'à 7 % les prix du papier co ...

Domtar démarre une nouvelle usine de CCP à l'usine de Nekoosa

En partenariat avec Omya, l'un des principaux producteurs mondiaux de minéraux essentiels et distributeur mondial de ...

Royaume-Uni : Le projet "tissue" à Goole de Metsä est en bonne voie

Metsä Tissue a déposé sa demande de planification finale pour un projet d'usine de tissue &agra ...

Arrêt de 10 jours pour maintenance chez Fibre Excellence Provence

L'arrêt pour maintenance démarrera le 1er mars pour une dizaine de jours. Objectif : moderniser et fiabiliser l'us ...

Que faire de la MAP 6 endommagée de Norske Skog Saugbrugs ?

Des enquêtes sont actuellement en cours à l'usine de Saugbrugs de Norske Skog, en Norvège, pour décider d ...

Weig prévoit d'augmenter les prix à partir du 1er avril

Le fabricant de carton plat recyclé Weig a formulé des demandes d'augmentation des prix. Motifs invoqués : d ...

Nouvelle hausse de prix de Suzano

Le producteur brésilien de pâte Suzano, a annoncé une nouvelle augmentation des prix de la pâte de feuillus. Précisément, il ...

Felix Schoeller annonce des suppressions d'emplois

Jusqu'à 210 emplois sur différents sites du fabricant de papiers spéciaux (photo, décoration...) Felix Schoeller sont ac ...

La nouvelle MAP d'ICT France à Pannes a démarré sa production

Mercredi 19 février, la deuxième ligne de production de l'usine ICT France (qui fabrique, commercialise et distribue en France la marque Foxy) a ainsi été inaugur&e ...

Pulpex finance la construction d'une usine de bouteilles à base de fibre en Écosse

Le britannique Pulpex, la société de technologie d'emballage durable lève 62 ...

Avec la fermeture prévue de l'usine de Penig dans les mois à venir, le groupe Felix Schoeller entend adapter ses capacités de production européennes de papiers ...

Une nouvelle machine de transformation TouchMax Gambini chez MPH1865

Cet équipement est une pièce unique à plus d’un titre : il s’agit non seulement du 100ème ...

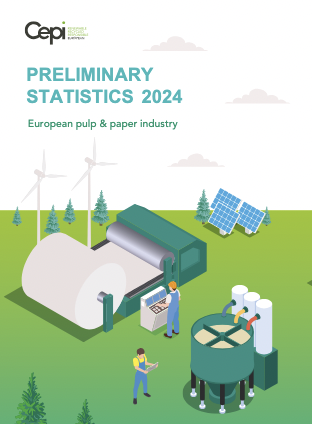

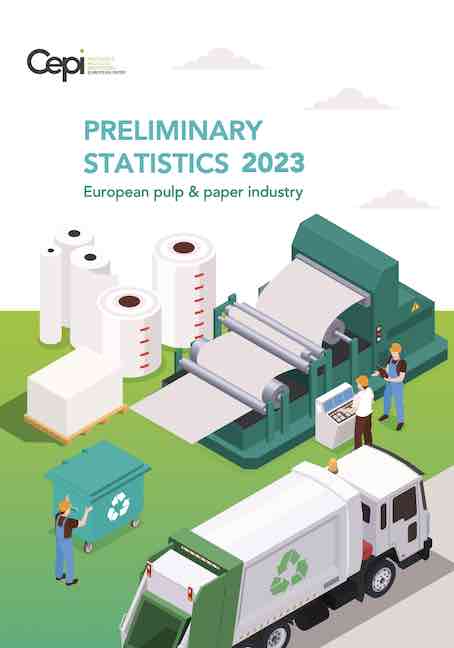

Rapport Cepi : La production de papier et de carton a augmenté de 5,2% en Europe en 2024

2024, une année résiliente pour le secteur européen de la pâte et du papier, comme le montre le rapport statistique préliminaire du Cepi. La consommation de p ...

Heinzel annonce une augmentation de prix pour Starkraft

Le groupe autrichien Heinzel a annoncé son intention d'augmenter les prix de sa marque de papier kraft Starkraft de 5 à 8 % &agra ...

Stora Enso Packaging Materials statue sur les licenciements temporaires en Finlande

Le groupe finno-suédois Stora Enso a finalisé les négociations statutaires avec les repr& ...

Bilan : Record de ventes en 2024 pour le géant brésilien Suzano

Bon bilan pour Suzano, qui valide sa stratégie ! Les ventes de pâte et de papier ont ainsi atteint un nouveau record de 12,3 millions de tonnes, en hausse de 7 % par rapport &agra ...

Nouvelle-Zélande : OjiFS va stopper la production de papier à son usine de Kinleith

"Après un travail approfondi et compte tenu d'une variété d'options et de commen ...

International Paper (IP) fermera quatre usines aux États-Unis

Rationalisation en cours chez l'américain IP qui annonce la fermeture de 4 sites aux Etats-Unis d'ici fin avril 2025, dont l'usine de carton ondulé de Red River. Celle-ci est une ...

Sylvamo va investir 145 M$ en Caroline du Sud

Les annonces des papetiers se suivent mais ne se ressemblent pas. Cette fois, c'est d'investissement dont il s'agit, avec Sylvamo. La sociét& ...

Cartiera Olona augmente ses tarifs

Après Paper Board Alliance et Cartiera Merati, c'est au tour de Cartiera Olona d'annoncer des prix plus élevés. À partir du 3 mars, ...

Regina roule pour le Giro d'Italie

Beau contrat de sponsoring que celui signé par Regina, la marque la plus connue du groupe Sofidel, l'un des leaders mondiaux dans la production de papier &ag ...

Metsä Tissue poursuit ses projets pour une nouvelle usine de tissue au Royaume-Uni

La division papiers de soie du groupe Metsä, Metsä Tissue, a soumis une demande de planification complète pour une nouvelle usine de papier de soie à Goole, en Grande-B ...

Le Groupe Klingele signe avec Maistapack et cède Onboard Corrugated

Le fournisseur de solutions de papier et d'emballage en carton ondulé, Klingele Paper & Packaging, conclu ...

Metsä Fibre envisage du chômage technique dans plusieurs scieries

Metsä Fibre pourrait réduire la production de certaines de ses scieries et procéder à des l ...

Finlande : UPM a repris la production à Kymi

L'entreprise finlandaise de produits forestiers UPM a repris la production à l'usine de pâte UPM Kymi à Kouvola aprè ...

Donald Trump signe un décret pour le retour des pailles en plastique

Le nouveau président des États-Unis, Donald Trump, ne sait plus quoi faire pour choquer : Après avoir ...

La machine RCCM chez Eren Paper démarrera début 2026

Eren Paper, une filiale d'Eren, avait acquis en 2021 auprès d'UPM le site de l'usine de papier Shotton, dans le nord du Pays ...

International Paper va construire une usine de 260 millions de dollars dans l'Iowa

Décidément International Paper, qui vient de fusionner avec DS Smith, ne reste pas en place ! Dernière initiative en date : l'acquisition d'un terrain à Waterloo, d ...

Butterfly Packaging acquiert Adrène

La concentration est de mise dans l'emballage, et ce quelque soit la taille des entreprises. Dernièrement, c'est Butterly Packaging (CA de 26 mi ...

Et si Metsä produisait des emballages souples à Husum en 2027 ?

C'est en tout cas en réflexion : Le papetier finlandais lance en effet une étude de préingénier ...

L'année 2025 démarre avec une méga fusion actée, symbole de la concentration encours dans le secteur de l'emballage : Celle du britannique DS Smith qui intèg ...

L'usine de pâte à papier UPM Kymi est temporairement en panne

La grève industrielle en cours dans l'industrie chimique en Finlande a contraint UPM à suspendre la produ ...

Jussi Vanhanen est le nouveau Pdg du groupe Metsä

Nouvelle nomination dans la filière, celle de Jussi Vanhanen qui a été nommé nouveau Pdg du groupe Metsä. ...

En plein C!Print, UPM annonce le rachat de Metamark

C'est la grande annonce qui est tombée durant le salon : UPM Raflatac acquiert Metamark. Son objectif : Faire d'UPM Raflatac un acteur important dans le segment graphique en croissance ...

L'autrichien Lenzing Papier expose pour la première fois au C!Print

Premium et papier recyclé ne sont pas incompatibles, c'est ce que veut démontrer le groupe autrichien Lenzing ...

Clap de fin pour La Papeterie Lecas

Le choix de la délocalisation a été fait par le groupe Hamelin, qui a décidé de fermer son site de production "la papeterie ...

L'Association des produits forestiers du Canada réagit

Même dans la filière, le bulldozer Trump fait des ravages ! L'Association des produits forestiers du Canada (APFC) réagit ainsi à la décision du pr&eacut ...

Intelligence artificielle, personnalisation, packaging, automatisation, impression responsable, cybersécurité... Beaucoup de sujets d'importance sont traités dans cette 12 ...

Mondi x zwiesel Glas : Une collab pour emballer du cristal

Mondi a collaboré avec Zwiesel Glas, un producteur bavarois de verrerie en cristal de haute qualité, pour développer un ...

UPM et Inapa France concluent un partenariat pour la distribution de papiers d’impression

Dans le cadre de cet accord, Inapa France assurera la distribution de plusieurs gammes de produits UPM, ...

Les prix augmentent ! Encore une nouvelle annonce ! Cette fois, c'est la société suédoise SCA qui a fait part de son intention d'augmenter les prix du papier kraft br ...

Autriche : Klingele Paper & Packaging s'associe avec l'entreprise familiale Maistapack

Ce partenariat va permettre au fournisseur de solutions de papier et d'emballage en carton ondulé d'e ...

Premièrement, c'est le site de Oudegem qui se verra attribué une machine Bobst 4 couleurs. Sa mise en service est prévue pour le début du mois d'avril 2025. Le seco ...

Ce n'est un secret pour personne, la situation économique en Allemagne se caractérise actuellement par de nombreux défis. Les exigences sur le marché des display on ...

Moins de 8 mois après son OPA sur Orapi, Groupe Paredes-Orapi a achevé sa réorganisation

GPO, nouveau N°1 intégré de l’hygiène professionnelle en France, annonce la sortie de bourse de sa filiale Orapi suite à une offre publique de retrait obl ...

VPK UK & Ireland va fermer son site d'emballage à Leeds, en Grande-Bretagne

L'usine de Leeds compte actuellement 59 employés et est spécialisée dans la production de s ...

Un incendie spectaculaire a ravagé l'usine de recyclage de Paprec à Amiens

Environ 11.000 m² de l'usine de recyclage de déchets Paprec ont été ravag&eacut ...

Chine : Hengan International a mis en service une nouvelle machine à tissue à Fujian

Le principal producteur chinois de papiers-mouchoirs Hengan International, qui existe depuis 1985, a ...

Lyreco renforce son positionnement d'apporteur de solutions pour les professionnels

Lyreco, leader de la distribution de produits et de services pour l’environnement de travail, annonce la cr&e ...

Nouvelle opération de croissance externe pour Labelys. Cette fois, il rachète Etiquel (14 millions d'euros de chiffre d'affaires annuel), une société portugaise sp& ...

L'usine de Sarreguemines de MM Packaging va fermer ses portes

Début d'année compliqué pour le groupe autrichien Mayr-Melnhof, contraint d'annoncer l'arrêt de son usine fran ...

Carton ondulé : IP investit 260 M$ dans une usine à Waterloo

Décidément, International Paper n'arrête pas ! Le groupe annonce la construction d'une usine de pro ...

Russie : JSC Kappa Rus rachète Okulovskaya Paper

JSC Kappa Rus reprend une usine de papier russe pour le papier ondulé. Précisément, celle-ci produit du papier ondul& ...

Feu vert de la Commission Européenne pour le rachat du britannique DS Smith par l'américain IP

La Commission Européenne a publié sa décision d'autoriser le rapprochement entre International Paper (IP) et le groupe britannique DS Smith. La fusion, d'un montant de 7,2 ...

Suzano procède à une augmentation de prix

Le premier producteur mondial de pâte à papier, a annoncé de fortes hausses de prix à partir de février. C'es ...

Sun Paper investit dans des systèmes de préparation de pâte et une ligne de pâte à papier à Nanning en Chine

Andritz a reçu une commande de Sun Pap ...

Rossmann va créer une nouvelle usine de carton alvéolaire

18 millions d’euros : c'est la somme que compte investir le groupe Rossmann dans une nouvelle usine de 10 000 m2, à proximité immédiate de son site de production d ...

Suède : Magnus Groth annonce qu'il quittera Essity en 2025

Une page va se tourner en 2025 chez le groupe suédois Essity, avec le départ prochain de son Pdg Magnus Groth. Il aura ...

GF Smith est le distributeur exclusif des papiers Gmund au Royaume-Uni

Nouveau challenge pour GF Smith qui ajoute la gamme Gmund à son portefeuille au Royaume-Uni. Il devient ainsi l'unique fo ...

Le site Tetra Pak de Longvic est menacé de fermeture

L'annonce a fait grand bruit en Bourgogne : Le leader mondial des briques Tetra Pak pourrait fermer son usine installée près de Dijon. Motifs invoqués : baisse des vo ...

Nova Paper acquiert Onboard Corrugated

La société néerlandaise Nova Paper, filiale du groupe Turc Eren, a acquis 100% des actions d'Onboard basé à Wolverhampto ...

Une étude de l'Ademe ne permet pas de conclure que réduire les prospectus est moins polluant.

Le rapport d’évaluation de l'expérimentation (143 pages !) du "Oui ...

Nordic Paper signe un nouvel accord de financement

L'année démarre sous le signe du changement pour Nordic Paper qui vient de conclure un nouvel accord de financement. Les nouvelles facilités de crédit comprenn ...

Autriche : L'entreprise familiale Bayer Kartonagen fait désormais partie de Schwarzach Packaging

La production de l'expert en emballages en carton de Lustenau est transférée chez ...

Procter & Gamble accusé d'éco-blanchiment

Une action en justice est menée contre le géant américain des produits de soins et de nettoyage Procter & Gam ...

Metsä Board, une filiale du groupe Metsä, a annoncé son intention de fermer son usine de carton de Tako et d'améliorer l'efficacité opérationnelle de l'usine de c ...

Le producteur allemand de carton JST abandonne son projet d'extension de capacités

JST ne poursuivra pas son projet d'installation d'une nouvelle machine à carton ondulé recycl&e ...

VPK lance VPK REflex

Le groupe belge VPK, sous la houlette de son Président, Pierre Macharis, a lancé son calculateur d'empreinte carbone produit pour permettre aux clients de faire des ...

Espagne : l'italien RDM veut fermer son usine à papier de Castellbisbal

Le groupe Reno de Medici (RDM) a annoncé son intention d'arrêter la production de son usine de Castellbisbal, près de Barcelone. L'usine, qui a la capacité de produi ...

Isabelle Erb-Polouchine présidente de la CCFI

L'AG de la CCFI s'est tenue hier mercredi soir à l'Ecole Militaire à Paris et a entériné les comptes de l'association. ...

Pro-Gest entame un processus pour surmonter la crise financière

L'année 2025 s'annonce compliquée pour bon nombre de dirigeants et l'italien Pro-Gest ne fait pas exception & ...

La plasturgie retrouve de la voix avec Polyvia

Pierre-Jean Leduc, le président de Polyvia l'a dit sans détour lors de la présentation effectuée par Polyvia mercredi matin ...

Papiers de sécurité : L'allemand Drewsen Spezialpapiere acquiert le britannique Portals Papers

Voilà une opération de croissance externe qui ne passe pas inaperçue : Le premier fabricant allemand de papiers de sécurité, Drewsen Spezialpapiere rach ...

Le britannique Macfarlane acquiert le groupe Pitreavie

Ce dernier, fondé en 2005, est spécialisé dans la fabrication et la distribution d'emballages de protection destin&eac ...

Victory Packaging devient Smurfit Westrock Packaging Solutions

Depuis plus de 50 ans, Victory Packaging s'est bâtie un héritage en matière de fourniture d'emballages et de se ...

Kolbus est repris par le fonds d’investissements industriels allemand Max Valier Holdings

Précisément, l’acquisition de la société mère Kolbus et de tou ...

Taurrus est une imprimerie de labeur, dotée d’un fort ancrage à Cavaillon (84) et dans la région PACA. Avec ses plus de 100 ans d’expérience cumul&eacut ...

Le suisse Bourquin poursuit le développement de son site de production à Oensingen

Une onduleuse nouvelle génération (marque BHS Corrugated) est arrivée sur le site ...

Hubergroup : l'Office fédéral allemand des cartels autorise son rachat par un consortium

Les nouveaux propriétaires du fabricant allemand d'encres d'imprimerie sont un consortium ...

Metsä Tissue renforce la compétitivité de son usine de Kreuzau

Pas de compétitivité sans investissements : c'est l'adage que Metsä Tissue, la division tissue du groupe Metsä, reprend à son compte en annonçant un plan ...

UPM Raflatac s'associe à Highlands pour étendre sa présence sur le marché britannique

Concrètement, l'agence internationale de vente, de marketing et de commerce &e ...

Brésil : Afry remporte le projet EPCM pour la nouvelle usine de pâte à papier d'Arauco

Arauco, une entreprise mondiale de l'industrie forestière, a attribué à ...

Georgia-Pacific investit 90 M$ pour développer son activité de papiers-mouchoirs grand public

L'investissement dans l'usine de Crossett créera 50 nouveaux emplois et augmentera l ...

Allemagne : La papeterie Meldorf de Tornesch a cessé ses activités fin 2024

Le processus d'investissement lancé dans le but de trouver un repreneur approprié pour l'entrep ...

Royaume-Uni : L'espagnol Alzamora Group rachète Offset Print & Packaging

Concentration encore et toujours dans l'emballage : Cette fois, c'est le fabricant Alzamora, spécialiste des solutions d’emballage en carton, qui reprend Offset Print & Packag ...

Les agréments sont prolongés pour 5 ans

Le 31 décembre 2029 : c'est la date à laquelle expirent les agréments qui viennent d'être prolongés pour Citeo, ...

Duni vient de signer un accord pour acquérir le fournisseur de solutions de vaisselle en papier Poppies Europe Ltd (Poppies). Cette fusion stratégique renforce la position d ...

Novolex acquiert Pactiv Evergreen pour 6,7 milliards de dollars

L'industrie de l'emballage se consolide toujours plus ! Novolex, un important groupe américain d'emballages pour l'alimentaire e ...

Lessebo Paper étend son partenariat avec Igepa Belux

Du nouveau dans la collaboration entre le papetier suédois Lessebo Paper et Igepa Belux, fournisseur de supports de communicati ...

La Commission européenne autorise l'acquisition d'APP par Jackson Wijaya, propriétaire de Paper Excellence

Fin d'année fructueuse pour Jackson Wijaya, propriétaire de Pape ...

Le groupe autrichien Mayr-Melnhof se sépare du groupe Tann

Mayr-Melnhof (MM), qui propose des solutions d'emballage pour le carton et le carton plat avec une offre attractive de papiers kraft, ...

Mondi Neusiedler investit 20 millions d'euros dans des sites plus durables

Le papetier Mondi a bien progressé dans son programme d'investissements de 20 millions d'euros pour ses usines de pap ...

Le papetier Sud-africain Neopak accélère sa digitalisation avec ABB

Neopak, l'un des principaux fabricants d’Afrique du Sud de carton pour emballages et de produits en papier, a r ...

Allemagne : Seaman Paper acquiert le fabricant de papier Julius Glatz

Seaman Paper, une entreprise familiale de quatrième génération, spécialisée dans les solutions ...

Suzano inaugure officiellement la plus grande usine de pâte à ligne unique au monde

Suzano, le plus grand producteur mondial de pâte à papier, a officiellement inaugur& ...

La Fefco salue l'adoption de la PPWR

La Fefco, Fédération européenne des fabricants de carton ondulé, salue l'adoption du Règlement sur les emballages et les d&eacu ...

Paprec devient le leader du recyclage en Suisse

No limit à l'expansion de Paprec ! Passé en 30 ans de 45 à 16 000 collaborateurs et collaboratrices répartis sur plus ...

L'italien Carton Pack acquiert deux sociétés d'emballages coup sur coup

Carton Pack, spécialisée dans la production d'emballages pour l'industrie alimentaire, a d'abo ...

Turquie : Les débuts de la nouvelle MAP 3 de Kipas Kagit à l'usine de Söke

La société turque Kipas Kagit a commencé les essais de sa nouvelle machine à ...

Metsä Board a finalisé les négociations sur le chômage technique en Finlande

Les négociations de changement de Metsä Board sur des licenciements temporaires ...

Produits Kruger étudie la construction d'une nouvelle usine de papiers-mouchoirs

Produits Kruger annonce qu'après le démarrage réussi de sa nouvelle usine de tissue & ...

Le belge Van Genechten Packaging (VGP) acquiert l'allemand Schoepe Display

VGP poursuit sa stratégie de croissance externe. Après avoir récemment acquis Dot2Dot en Pologne, l'en ...

Un incendie massif s'est déclaré hier matin à l'usine de papier Sapphire de Fourstones à Leslie, en Écosse

L'usine a actuellement la capacité de produire 30 ...

La 1ère édition nationale de la Matinale des Paperteams s'est tenue le 10 décembre à Paris

Cette manifestation était animée par l’IPC. Elle a rassembl& ...

Mayr-Melnhof investit dans l'usine de Gernsbach et nomme un nouveau directeur général

L'usine MM Gernsbach, qui peut produire jusqu'à 280 kt de carton recyclé couché ...

Wepa demande une nouvelle MT sur le site de Bridgend

Après que le fabricant allemand de papiers-mouchoirs Wepa ait installé une nouvelle machine à mouchoirs (capacité ...

Oji Fibre Solutions envisage d'arrêter la production à Kinleith en Nouvelle-Zélande

Kinleith Mill est la plus grande usine de fabrication de pâte et de papier d'Oji Fibre So ...

Programme BIORAF : Former des ingénieurs pour une bioéconomie durable

Conçu en partenariat par Grenoble INP - UGA (via Grenoble INP - Pagora et Grenoble INP - Géni ...

Le belge VPK vend deux de ses sites français au groupe TNM Emballage

Du nouveau chez le groupe belge VPK qui vient d'annoncer la cession de ses sites des Echets (Rhône) et de Groisy ...

Ahlstrom investit 15 M€ à St-Séverin, dans la dernière papeterie de Charente

A Saint-Séverin, le papetier finlandais Ahlstrom investit 15 millions d'euros pour u ...

UPM Fibres procède à des ajustements d'effectifs

UPM Fibres a achevé les négociations avec les syndicats et supprimera un maximum de 88 emplois. L'entreprise et les r ...

Toscotec achève son deuxième projet de reconstruction chez Ranheim Paper & Board en Norvège

Après une reconstruction réussie de la section séchoir fourni ...

DS Smith investit 34 millions d'euros en Hongrie

Cet investissement améliorera les opérations sur des sites clés à Füzesabony, Nagykáta (modernisation de l'ond ...

Rengo revoit à la hausse les prix de son carton duplex couché

L’environnement commercial autour des panneaux duplex couchés est très difficile en raison de la flamb& ...

Le groupe Japonais Ovol Japan Pulp&Paper finalise l’acquisition d’Inapa France

Voilà une opération qui fut promptement menée ! Le groupe Japonais Ovol Japan Pu ...

Billerud rejoint la plateforme Industrikraft en Suède

Industrikraft est une plateforme où les entreprises industrielles suédoises collaborent pour garantir un approvisionnement e ...

Grâce à sa reconstruction, la MAP 4 de DS Smith à Viana est pleinement opérationnelle

Le cartonnier britannique DS Smith a de quoi être satisfait : la reconstruc ...

Kleenex lève un voile sur son nouveau logo

400 000 boîtes de Kleenex (groupe américain Kimberly-Clark) sortent quotidiennement de l’usine de Sotteville-lès-Rouen ...

Carton couché : RDM augmente ses prix

Le groupe Reno de Medici (RDM) souhaite augmenter les prix de toutes les qualités de carton couché de 50 €/t. L’augmentation ...

UPM Raflatac va fermer l'usine de Kaltenkirchen en Allemagne

UPM Raflatac a annoncé la fermeture de son usine de Kaltenkirchen, près de Hambourg, en Allemagne. Le site fabrique des ...

Federec prend un nouvel "R"

À l’occasion de son Assemblée générale extraordinaire qui s’est tenue sur le salon Pollutec Paris, le salon international des solut ...

Arrêt définitif de la MAP 3 à l'usine d'UPM Nordland Papier Dörpen

UPM Communication Papers a fait état de l'arrêt permanent de sa machine à papier fin, l ...

Saica explore le projet d'usine de papier recyclé à Dayton, dans l'Ohio

L'espagnol Saica part à la conquête de l'Amérique ! Le producteur de papier recyclé et ...

Le consortium de MAVCO Investments et Avenue Capital Group signent un accord pour acquérir l'allemand Hubergroup

Du nouveau dans le secteur de l'impression et de l'emballage ! Le fabricant allemand d'encres d'imprimerie (et de produits chimiques) a signé avec MAVCO Investments, un fonds d'investissement a ...

Laakirchen Papier stoppe la production de papier SC fin novembre

Laakirchen Papier, qui fait partie du groupe autrichien Heinzel, arrêtera la production de papier SC à partir de fin ...

Espagne : Hinojosa Packaging confie à Voith la reconstruction de sa MAP 1 à Alquería

Le projet vise à augmenter la production de carton-caisse avec des grammages de 115 &a ...

Metapaper est le nouveau distributeur pour Lessebo Design et Lessebo Colors

Metapaper devient distributeur de Lessebo Design et Lessebo Colors en Allemagne, Autriche et France. Ces gammes de papier h ...

SCA a achevé la modernisation de son site d’Ortviken, en Suède

Ce chantier a permis de tripler la capacité annuelle de production de pâte chimio-thermomecanique (CTMP) sur le site de SCA, passant de 100 000 à 300 000 tonnes. On ra ...

VPK confie à FMW Industries la fourniture d'une ligne d'alimentation de pulpeur OCC en Belgique

Cette collaboration importante s’appuie sur l’expérience réussie de FM ...

Finlande : L'usine de Kuopio de Mondi relancera sa production avant Noël

La production a été interrompue le 4 novembre lorsqu'une explosion dans la tour de pâte à papi ...

Le Groupement des Hôtelleries et Restaurations de France a signé un partenariat avec Citeo Pro

Pas facile pour les restaurateurs de s'y retrouver dans les réglementations qui les ...

MPH1865 acquiert les actifs des Laboratoires Prodene Klint (LPK)

MPH1865 (anciennement MP hygiène), entreprise référente dans la fabrication et la transformation de produits d'hy ...

ICT France va démarrer une nouvelle machine à mouchoirs début 2025

Le fabricant de tissue ICT France est en bonne voie de finaliser son projet d'expansion. L'entreprise est ...

Mondi a démarré sa nouvelle ligne d'extrusion à l'usine de Štĕti en République tchèque

Le chantier comprend également la construction d'un nouveau bâtiment de production équipé de machines de revêtement. Mondi affirme que le projet permet d'&eacu ...

La production de plastique baisse en Europe

8,3 % : C'est la chute de la production européenne de plastiques (UE + Suisse, Norvège et Royaume Uni), qui est tombée à 54 mil ...

Metsä Board modernise son usine de Simpele

Metsä Board poursuit son investissement visant à moderniser l'usine de carton plat pliant de Simpele, en se concentrant sur l'am&eacut ...

Albany International veut consolider sa capacité de fabrication

Heimbach, une filiale d'Albany International, a annoncé qu'elle entamait des consultations avec les représentants ...

Le britannique DS Smith investit plus de 25 M€ dans ses sites en Pologne

DS Smith poursuit son développement en Europe centrale et orientale avec un investissement de plus de 25 millions d’euros dans ses installations existantes en Pologne. Le gro ...

Portugal : La reconstruction de l'usine DS Smith de Viana est terminée

La MAP 4 de l'usine de papier DS Smith de Viana, au Portugal, a terminé sa reconstruction et a redémar ...

Un nouveau logo pour le Conseil National de l'Emballage

27 ans après sa mise en service, l’identité visuelle du Conseil National de l’Emballage (CNE) évolue. Si l&rsq ...

L'autrichien Lenzing investit dans les fibres cellulosiques du suédois TreeToTextile

Le fabricant autrichien des fibres cellulosiques Lenzing prend une participation minoritaire dans Tree ...

La Fipec alerte sur la hausse des coûts et la baisse de la demande

La fin d'année est morose et la Fipec, qui rassemble les fabricants français de peintures, encres, colles, adhésifs et résines ne cache pas ses inquiétudes p ...

Ryam lève 67 millions d'euros

Le financement se découpe de la manière suivante : 37 millions d’euros de prêts à terme garantis proviennent des banques fran&cce ...

C'est fini pour la papeterie de Stenpa (contraction de Stenay et de « papers ») et ses 124 collaborateurs. Le tribunal de commerce de Bar-le-Duc vient de prononcer sa liq ...

Mondi a finalisé un investissement de 90 M€ dans son usine de Mszczonów, près de Varsovie

Celle-ci a doublé sa capacité, ce qui en fait la plus grande usine de ...

ABB fournit de nouveaux équipements à DS Smith Paper Italia

C'est le site DS Smith Lucca qui va accueillir le nouvel équipement d'ABB, un système d'entraînement &agr ...

Les résultats financiers de Sappi pour le quatrième trimestre et l'année entière dépassent les attentes

Commentant les résultats du groupe, Steve Binnie, Pdg de Sappi, a déclaré : "Après un bon dernier trimestre, je suis heureux que nous ayons pu dépasser ...

Algérie : Toscotec fournira une ligne de production de tissue au groupe Wafa

Le producteur algérien de papier tissue Wafa a retenu l'italien Toscotec pour la fourniture d'une nouve ...

Le rachat de Schumacher Packaging en Pologne par Saica a été validé par les autorités polonaises de la Concurrence

Opération de croissance externe finalisée ...

Les sacs plastique ne sont plus taxés en Suède

Sous l’influence d’un parti d’extrême-droite, le gouvernement libéral conservateur a abrogé une disp ...

Annulation du décret emballages plastiques fruits & légumes

Dans un autre genre, l'Administration française se distingue aussi en autorisant de nouveau les fabricants d&rsquo ...

Inde : Un nouvel équipement Runtech pour la papeterie Silverton Pulp & Paper

La livraison comprend trois turbosoufflantes EP600 et des systèmes de mesure de déshydratation Ec ...

Finlande : Stora Enso vend les murs de son usine de Sunila à Kotka

Le papetier Stora Enso restera dans la propriété en tant que locataire d'Aalto Development, pour poursuivr ...

Etats-Unis : Domtar rachète Iconex Paper

Iconex Paper, auparavant détenu par Atlas Holdings, est spécialisé dans la transformation de bobines de papier thermique en roulea ...

Décidément, la Pologne devient the place to B ! Après Saica qui a racheté les usines de Schumacher Packaging en Pologne, c'est au tour du fabricant d'emballages&nbs ...

Italie : Labelys acquiert l'imprimerie Perrucio

Concentration toujours dans le secteur des étiquettes avec cette opération réalisée par le groupe Labelys présid&eac ...

Aldar Tissues ouvre une nouvelle usine à Dublin

Aldar Tissues, fabricant irlandais de papier de soie, faisant partie du groupe Zeus, a inauguré sa nouvelle usine à Rathcoole, (Du ...

Sylvamo et IP mettent fin à leur accord d'approvisionnement avec l'usine de Georgetown

Sylvamo et International Paper mettent fin à un accord d'approvisionnement en papiers à ...

Clearwater Paper annonce la clôture de la vente de son activité tissue

Clearwater Paper a annoncé la finalisation de la vente de son activité papier-mouchoir à ...

L'allemand Palm rachète l'usine britannique de John Hargreaves

Le mois dernier, Palm a acquis 100 % des actions de John Hargreaves, une usine familiale basée à Stalybridge, ...

IP revoit ses options stratégiques pour son activité mondiale dans le secteur des fibres de cellulose

Grosse réflexion en cours chez le cartonnier américain, qui est en train de finaliser l’acquisition du britannique DS Smith ! « International Paper s'est engagé ...

Buckman augmente ses prix sur les produits de pâte et papier en Europe, au Moyen-Orient et en Afrique du Nord

Buckman, une entreprise chimique spécialisée basée aux &E ...

All4Pack Emballage Paris, retour sur la journée 1 !

6ème industrie en France et 7ème industrie mondiale, l'industrie de l'emballage est incontournable et se situe au coeur des en ...

Italie : Sphere rachète Romagnasac

Le groupe familial Sphere, qui a été repris récemment par le fonds Hivest Capital, acquiert, auprès du fonds d’investisseme ...

Metsä Tissue lance une nouvelle consultation publique pour son projet d'usine à Goole au Royaume-Uni

Dans les grandes lignes, il s'agirait de créer une usine capable de produire en ...

Le producteur espagnol de carton Iberboard est en cours de liquidation

Iberboard, qui a déposé son bilan cet été est en cours de liquidation. La fermeture affectera 80 emp ...

Emballages ménagers : Le fonds Hivest Capital acquiert le groupe familial Sphere

Fondé en 1976, le groupe familial aux 1 600 collaborateurs est repris par le fonds Hivest Capital. « Cette opération va nous permettre de nous structurer dans la conti ...

Finlande : Stora Enso rachète la scierie Junnikkala Oy

Pour sécuriser son approvisionnement en bois pour son site de production de carton d'emballages basé à Oulu, St ...

Ryam redémarre la ligne A sur son site de Jésup en Georgie

Rayonier Advanced Materials (RYAM), spécialiste des technologies basées sur la cellulose a annoncé l ...

Finlande : Chômage technique en vue chez Metsä Board

Le groupe Metsä Board entame des négociations sur d'éventuels chômages techniques au sein de son conseil ...

L’usine de papier à sac kraft Stambolijski de Mondi, en Bulgarie, touchée par un incendie, ne reprendra pas sa production. L'entreprise a annoncé qu'elle avait d&eac ...

Navigator met en service une nouvelle usine d'emballage en fibre moulée

Le producteur portugais de papier Navigator Company, a démarré sa nouvelle production de fibres d'emballage moulées dans les locaux de son usine de pâte à pap ...

Inauguration de l'usine de bioproduits Metsä Group Kemi

L'usine de bioproduits Kemi, d'une valeur d'environ 2 milliards d'euros, vient d'être inaugurée. Elle augmente les exportatio ...

On n'arrête plus Antalis dans sa course à la croissance ! Récemment, il avait ainsi repris les activités papier de Xerox dans la région EMEA (lire &agrav ...

Inapa France et sa filiale Inapa Loos sont officiellement reprises par Japan Pulp & Paper

La chose est désormais officialisée par un communiqué de l'entreprise : Inapa France ...

Alliance Etiquettes acquiert "impressions de l'Enclos"

Concentration toujours mais dans l'étiquette cette fois avec l'acquisition par Alliance Etiquettes de la société de pr ...

Espagne : Antalis rachète Plaesa, distributeur et transformateur hautement spécialisé dans l'emballage

Antalis continue ses opérations de croissance externe : cette fois, il acquiert l'entreprise familiale espagnole qui réalise un chiffre d'affaires annuel de 6 millions d'eur ...

Lancement de la Lettre de l’éco circulaire

Le premier numéro, imaginé par Carton Ondulé de France et CAP, ambitionne de lutter contre le dogmatisme en misant sur la ...

Les Papeteries de Condat sont à l'arrêt

Précisément, la ligne 8, la seule restante, est à l'arrêt depuis le 3 octobre. Et ce un an tout juste après le p ...

Riso vise le marché de l'emballage à All4pack

À l’occasion du salon All4Pack 2024, Riso présentera en avant-première Integlide, une solution d&rsquo ...

Huhtamaki étend sa capacité de production de couvercles en fibre à Lurgan, en Irlande du Nord

Le Finlandais Huhtamaki, producteur mondial d'emballages pour aliments et boissons, annonce le début de la production de fibres moulées lisses (SMF) dans son usine à Lurga ...